When you make a payment, it feels instant. But behind every card swipe, mobile tap, or online checkout, there's a robust infrastructure ensuring that transactions move securely, accurately, and efficiently. For issuers and acquirers, understanding how these systems work is critical—not just for resolving exceptions or monitoring performance, but also for identifying opportunities to improve authorization rates, reduce fraud, and optimize routing.

Visa and Mastercard operate the two most important networks in global payments: VisaNet and Banknet. Each is built to support massive transaction volumes at scale, with built-in resilience, security, and real-time capabilities that make them essential to modern commerce. In this blog, we break down how these networks operate, and how issuers and acquirers can benefit from understanding their architecture and functionality.

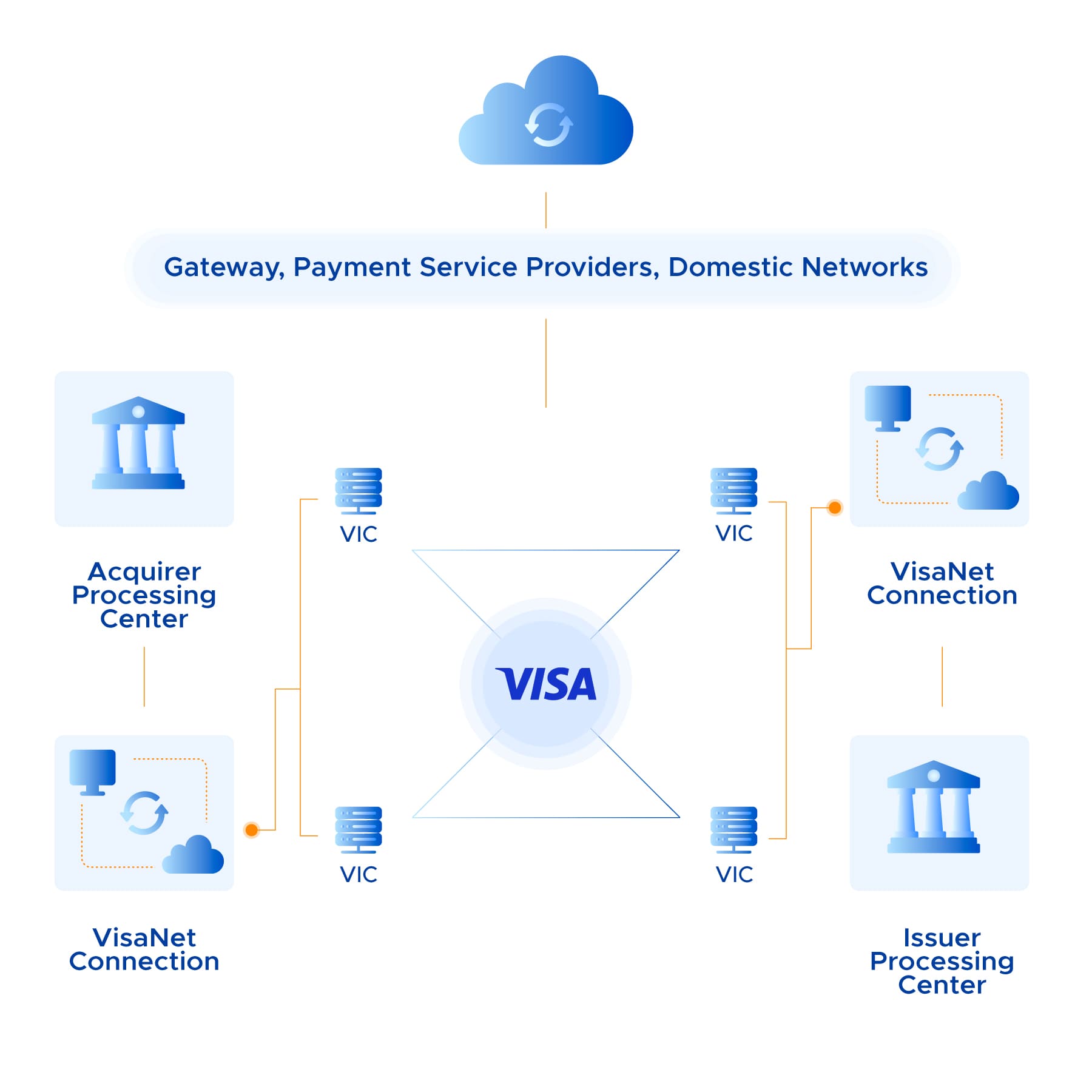

What is VisaNet and how it supports secure transaction processing

VisaNet is the global processing network developed by Visa to support the end-to-end lifecycle of card transactions—from authorization and clearing to settlement and dispute resolution. It serves as the digital backbone that connects issuers, acquirers, merchants, and third-party processors.

VisaNet is not just a messaging system; it's an intelligent, dynamic engine that helps route transactions optimally, applies risk management logic, and ensures availability even in high-volume or disrupted environments.

Main features of VisaNet for issuers and acquirers

Visa processing centers (VICs): These centers operate globally to ensure transactions are processed 24/7 without interruption.

End-to-end encryption: Cardholder data is encrypted throughout the journey, helping prevent data breaches and ensuring PCI compliance.

DEX and EAS connectivity: Visa offers direct exchange (DEX) and extended access (EAS) options to help issuers choose the best method of connection based on scale and performance needs.

Stand-in processing (STIP): If the issuer is temporarily unavailable, VisaNet can make real-time approval or decline decisions based on risk profiles and historical data, keeping the transaction flow uninterrupted.

VisaNet is also designed to support innovation. Its infrastructure accommodates tokenization, contactless payments, and emerging technologies, making it a future-ready system for any institution looking to modernize its transaction framework.

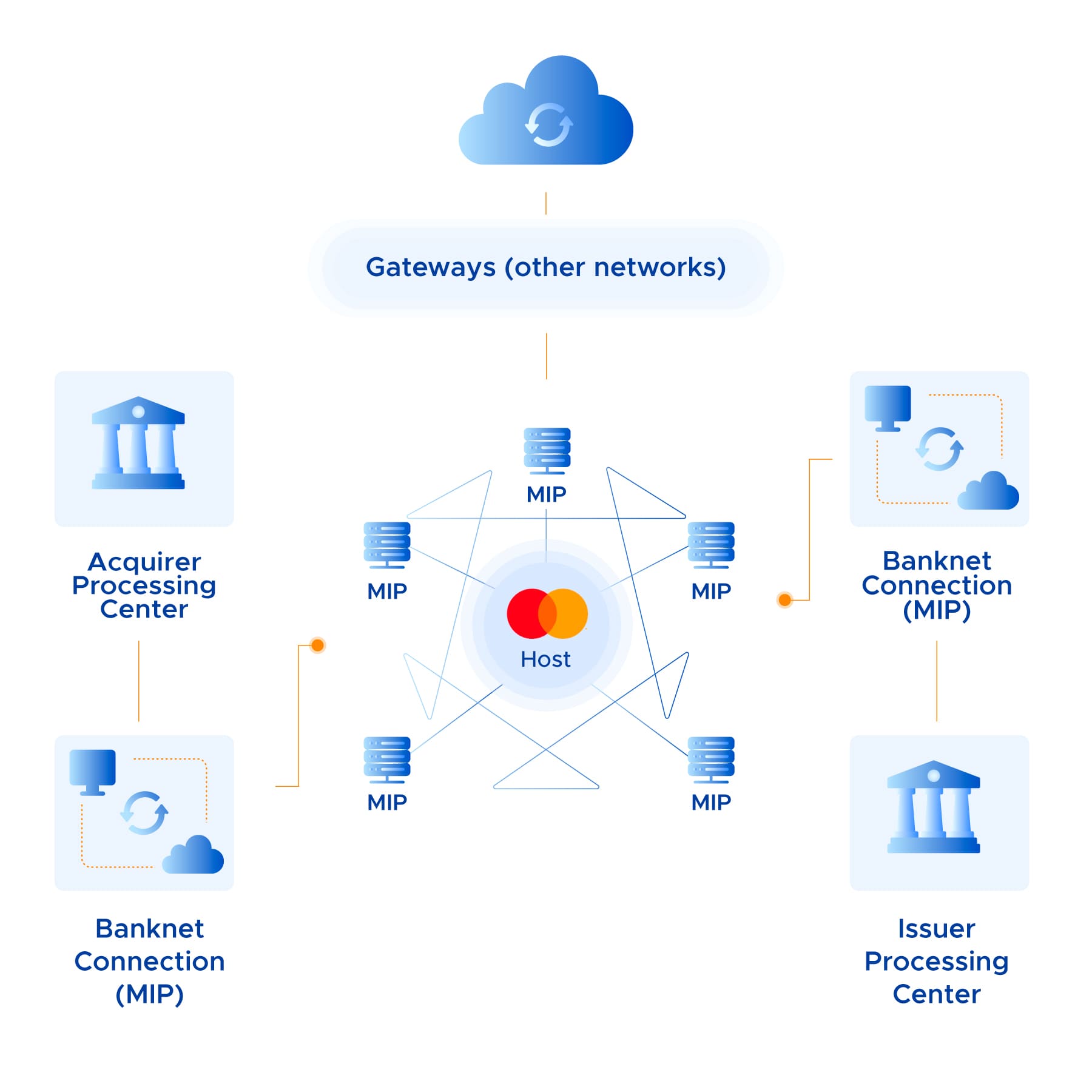

What is Banknet and how Mastercard processes global payments

Banknet is Mastercard's proprietary global communications network. It enables issuers, acquirers, and processors to exchange financial data with reliability and speed, powering millions of Mastercard transactions every day. Built to support interoperability and advanced routing, Banknet is critical to ensuring seamless card acceptance globally.

Where VisaNet is known for its scalability and intelligent routing, Banknet is equally renowned for its focus on resilience, interoperability, and flexible access points.

Main features of Banknet and how acquirers connect to Mastercard

Mastercard interface processor (MIP): MIP enables real-time message exchange and authorization with high performance and security.

Integrated stand-in services: Similar to Visa, Mastercard also provides stand-in functionality, ensuring cardholders experience minimal disruptions during network outages or processor issues.

Global switching capabilities: Banknet routes transactions across multiple regions, supporting local and cross-border transaction flows with high accuracy.

Multi-brand support: Banknet is built to process not only Mastercard-branded transactions but also those from co-branded and white-label programs, making it a highly flexible solution for global portfolios.

Banknet is also built for innovation. Its architecture supports digital-first use cases such as tokenized payments, mobile wallets, and omnichannel commerce, making it a flexible foundation for acquirers and issuers looking to expand into new markets or offer modern payment experiences.

How Visa and Mastercard ensure secure, real-time payment processing

Both networks are engineered for real-time processing at a global scale. They are constantly monitored for anomalies, latency, and threats, ensuring uptime and fraud mitigation. Here are key shared capabilities:

Real-time fraud detection using AI and historical data modeling

Tokenization to protect sensitive card data at every stage

Disaster recovery systems that automatically reroute transaction flows in the event of failure

Multi-layer authentication support, including 3DS and biometric integrations

This makes them ideal for supporting Card Not Present (CNP) transactions, mobile payments, and other fast-growing channels.

Why VisaNet and Banknet matter for issuers and acquirers

For issuers and acquirers, these networks are more than just communication highways—they are critical infrastructure. A strong understanding of how they operate allows you to:

Evaluate and improve authorization performance

Monitor and reduce transaction latency

Design failover systems that align with network architecture

Anticipate and prevent issues during peak processing times

Improve routing strategies and potentially reduce costs in high-volume segments

Moreover, many advanced features—such as STIP configuration, data enrichment, or fraud rules—require a network-level understanding to be fully optimized.

Optimizing payments with VisaNet and Banknet infrastructure

VisaNet and Banknet are the invisible engines behind seamless payments. But for issuers and acquirers, visibility into their design and function unlocks real opportunities. Whether you're launching new products, entering new markets, or refining your transaction strategy, your ability to operate confidently depends on how well you understand the networks supporting every authorization and settlement.

With their shared focus on speed, security, and scale, VisaNet and Banknet continue to evolve, offering powerful tools to those ready to engage with them more deeply.

This blog is intended for informational and educational purposes only and reflects Intelica's perspective based on our work with issuers and acquirers in the card payments space. It should not be considered professional advice. If you're exploring how these insights may apply to your organization, our team is available to help you assess your specific context.